Day 20 - Valentine 2025

Foolish Trader Journal, Day 20

Today ends Week 4 of this experiment. Disclaimer - the content here is not financial advice, it is entertainment. See my introductory post here.

Trading Update

I did not find anything exciting enough today as well. A reminder that I only have maybe 10 to 15 minutes in the day to actually think, decide, and act on an idea. This experiment is something I get a little time to spend on either before my day job starts or during my lunch hour. I am definitely not poring over charts or anything like that for the most parts of the day.

Anyway, I needed to begin freeing up some capital. To that end, today I closed my SOFI LEAP for a 5.5% profit, the position lasted 9 days.

I also opened a couple of AAPL downward hedge positions. I am sort of using AAPL as a loose proxy for the overall market. I just needed some protection and AAPL seems as big as any to fall if the overall market tanks. Why am I looking for protection? Well, amor fati - the love of one's fate!

A.I. on Hedging AAPL Stock with Protective Put Options

Before I opened my AAPL Hedge, I had asked Claude (from Anthropic) on how to go about it. Note that Claude did not suggest I do any of this, it was just me asking it how I would go about doing it. I thought this was entertaining!

Me

Question on Hedging.

I have 300 shares of AAPL.

Assume AAPL grows by 10% a year.

I need to buy 3 AAPL PUT Options to Hedge my position. I am trying to hedge against wild drops such as 20 - 50 percent drop in value due to unknown black swan style events.

To keep the costs low, what would be an ideal frequency to buy these options (i.e., bi-weekly/monthly/quarterly?)?

And what would be the ideal delta?

Claude

Let me help you think through the optimal hedging strategy for your AAPL position.

For hedging against black swan events (large drops of 20-50%), we need to balance protection with cost efficiency. Let's analyze this:

- Frequency Trade-off:

- Bi-weekly options: Highest time decay (theta), most expensive over time

- Monthly options: Moderate time decay, moderate cost

- Quarterly options: Lowest time decay per day, most cost-efficient for longer-term protection

For black swan protection, quarterly options would likely be most cost-effective because:

- You're protecting against rare events, not short-term volatility

- Longer-dated options have less theta decay per day

- Transaction costs are lower (4 trades per year vs 12 or 26)

- Delta Selection:

For black swan protection, you'd want to use out-of-the-money (OTM) puts:

- Delta around -0.20 to -0.30 would be optimal

- This provides good protection against major drops while keeping premium costs reasonable

- More negative deltas (like -0.40 or -0.50) would be too expensive for black swan protection

My recommendation:

- Buy quarterly puts with -0.25 delta

- Roll them about 2 weeks before expiration to avoid acceleration of theta decay

- This gives you consistent protection while managing costs

Would you like me to explain more about why this specific delta range would be optimal for your situation?

Note: This is general guidance - actual options strategies should consider your specific risk tolerance, tax situation, and market conditions.

Me

Are you able to evaluate how the above strategy would have performed in 2021?

Claude

Given my knowledge cutoff and without real-time market data, I can't provide exact performance numbers for 2021. However, I can explain what we know about AAPL's major movements in 2021 to help evaluate this strategy:

2021 AAPL Overview:

- AAPL started 2021 around $132

- Ended the year around $178

- Overall gain of approximately 35% for the year

- No major "black swan" drops occurred during this period

- The stock experienced normal market volatility but generally trended upward

In this scenario, the quarterly -0.25 delta put strategy would have:

- Generated consistent costs (premium paid for puts)

- These puts would have expired worthless since no major drops occurred

- The cost of the protection would have reduced your overall returns

This illustrates a key aspect of this hedging strategy: In strongly bullish years like 2021, it acts like an insurance policy - you pay the premiums but don't "use" the insurance. The strategy is designed to protect against severe downsides, not to enhance returns in bullish markets.

If you're interested in detailed performance analysis, you would need to:

- Get historical options pricing data for AAPL puts from 2021

- Calculate the actual premiums paid for each quarterly roll

- Factor in transaction costs

- Compare total costs against the protection provided

Would you like me to explain how to analyze the strategy's performance in years where significant drops did occur?

Me

That's good. How about year 2022?

Claude

2022 provides a much better test case for this hedging strategy since AAPL experienced significant declines:

2022 AAPL Key Movements:

- Started around $178

- Fell to around $130 by end of year

- Total decline of approximately 27% for the year

- Had several significant drops:

- March-June: ~28% decline

- August-September: ~20% decline

- September-January: ~15% decline

The quarterly -0.25 delta put strategy would have:

- Provided valuable protection during the major drawdowns

- The puts purchased in early 2022 would have moved into profit as AAPL declined

- Particularly beneficial during Q2 and Q3 when the largest drops occurred

- Some of these puts would have been worth exercising or selling for profit

The strategy would have helped mitigate losses by:

- Offsetting some of the stock's decline with put option profits

- Particularly effective during the sharp drops in Q2/Q3

- The -0.25 delta would have provided meaningful protection while not being too expensive

This scenario demonstrates when the "insurance policy" pays off - the cost of the puts would have been justified by the protection they provided during the significant market declines.

Would you like me to explore specific aspects of how the strategy would have performed during any particular period in 2022?

Me

Yes. Would quarterly hedging still have outperformed monthly hedging in terms of cost effectiveness?

Claude

For 2022's specific market conditions, let's analyze quarterly vs monthly hedging:

Monthly Hedging Advantages in 2022:

- Better ability to adjust strike prices to market conditions

- Could lower strikes as AAPL kept declining

- More opportunities to "reset" the hedge levels

- Particularly valuable during the sustained downtrend

- Greater flexibility during high volatility

- VIX was elevated throughout much of 2022

- Monthly adjustments allowed better response to changing market conditions

- Could capture profits on successful hedges more frequently

Quarterly Hedging Disadvantages in 2022:

- Longer-dated options were relatively expensive due to:

- High implied volatility environment

- Greater uncertainty about tech stocks

- Macro concerns (Fed tightening, inflation)

- Less optimal strike adjustment

- Stuck with higher strikes from before major declines

- Had to predict further out in an uncertain environment

- May have been over-hedged or under-hedged at times

In this specific case, monthly hedging likely would have been more cost-effective because:

- More frequent adjustments matched the trending nature of the decline

- Could better optimize strike prices to market conditions

- Shorter duration reduced the volatility premium paid

- Better ability to take profits on successful hedges

The key lesson is that in trending markets (versus sudden crashes), more frequent hedge adjustments can be advantageous despite higher transaction costs. Would you like me to explain how to determine when to switch between monthly and quarterly hedging based on market conditions?

All right, back to regular programming!

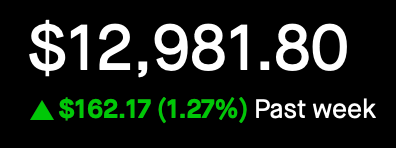

Portfolio Status

Here is the status of my open trades at the end of the day today.

The MSFT and GOOGL LEAPS continued to trend sideways today. The overall portfolio went down a bit today. I am still waiting for the LEAPS to hit my exit targets.

Here is a Year to date view of the portfolio.

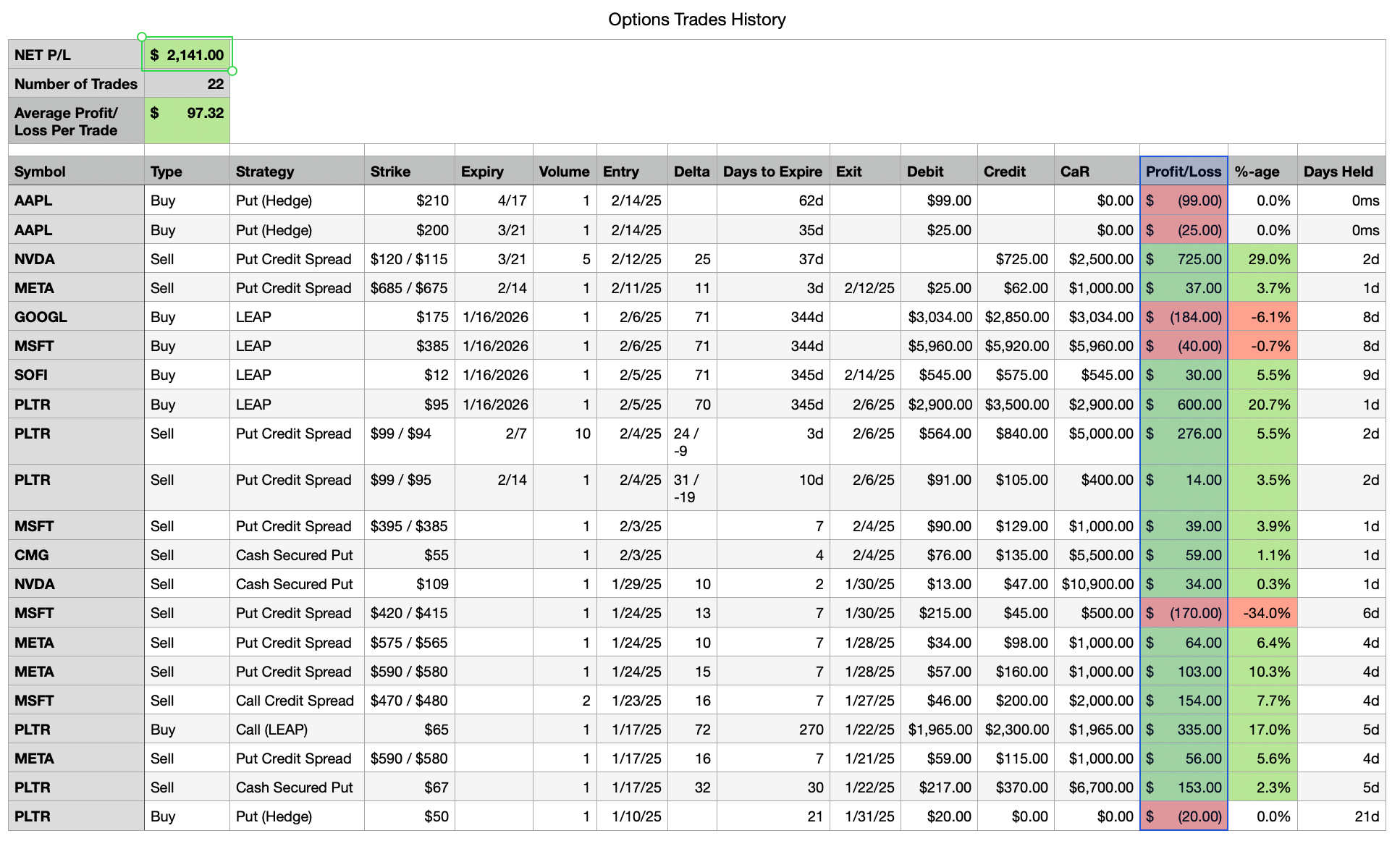

Trade History

Here is my trading history since I started recording my trades.

Week 4 Reflections

My trades didn't quite have as much volatility as I expected. A couple of days ago, I wrote how I am struggling to take on more risk. However, with most of the cash in the market, I am not sure I should really be thinking that way. My account barely moved since past week.

I am strongly convinced I have entered the right LEAPS. Still waiting for the market to begin moving MSFT and GOOGL northward. The game of cat and mouse with the market is truly on. Let's see who blinks first!